The Department of Defense (“DoD”) issued its final rule on January 31, 2023, made effective on the same date, implementing section 824 of the National Defense Authorization Act (“NDAA”) for fiscal year 2017. Significant to the new rule is the added requirement for CEOs to determine that the Independent Research and Development (“IR&D”) “will advance the needs of DoD for future technology and advanced capability as DoD describes such needs in communications referenced at 242.771-3(c)(1)(i)”. With the CEO now making the determination, requirements for the Administrative Contracting Officer (“ACO”) were removed.

Since the new rule is effective as of January 31, 2023, it will be important for major contractors with a calendar fiscal year to quickly evaluate their current practices for assessing and documenting IR&D projects of “potential interest” and adjust these practices to include the CEO’s review and determination that the IR&D projects will advance the needs of DoD. Major contractors are required to update the Defense Technical Information Center (“DTIC”) online input form no later than 3 months after their end of the fiscal year. Therefore, calendar fiscal year contractors will need to make these updates by the end of March 2023.

Documentation of the CEO’s assessment and determination will be important for supporting the allowability of the IR&D costs. It is very likely that during its ICS audits, DCAA will evaluate the allowability of IR&D considering the CEO’s determination. Without documentation of the determination there is significant risk that DCAA will deem these costs to be unallowable.

Chess Consulting has a team of professionals and leaders with decades of experience assisting clients and their outside legal counsel with complex government contract matters including accounting and regulatory compliance issues. Please contact us at https://chessconsultingllc.com/contact/ to see how we can assist.

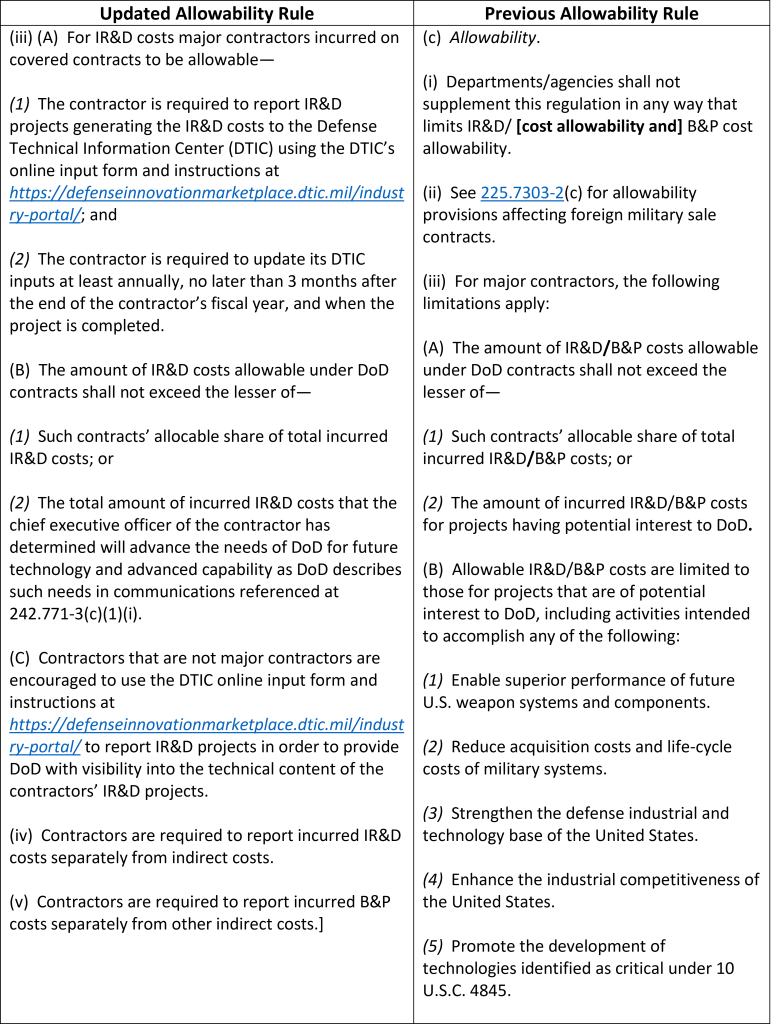

The table below lists relevant DFARS regulations for the prior and new rule for comparison.